After Alphabet announces earnings, there’s usually an easy-to-write article that decries how much Google is spending on “other bets”. I’ll be publishing a full analysis of Google’s earnings in a bit, but wanted to call out this topic as a particular injustice.

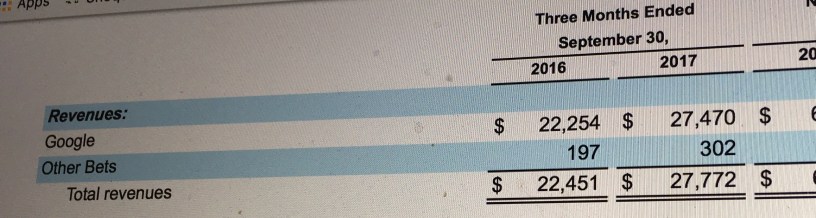

When Google announced their reorganization and creation of Alphabet (I had to check that it wasn’t April 1 that day…), they changed their reporting structure on their 10-k. They report Google per se vs. “Other bets” separately, making it easier to figure out what’s going on. The table below shows the results:

| 2016 | 2017 | ||

| Revenues | $16,089 | $19,723 | |

| Expenses | $(9,844) | $(12,125) | |

| Net Income | $6,245 | $7,598 | |

| Other Bets | Revenues | $197 | $302 |

| Expenses | $(1,058) | $(1,114) | |

| Net Income | $(861) | $(812) |

Simplistically, this shows that Google is a terrific business, and “other bets” is a horrific one. The resulting superficial storyline discusses this expenditure in a negative light.

This line of reasoning is absurd. Google should be applauded for their transparency here, which shows their investment level and how much it’s costing investors. If other tech companies followed suit, it’d appear similar or worse.

For example, Amazon – the king of opacity – hides everything in a few large buckets. How much are they spending on Echo, and Alexa, and Lab123 projects, and other investment areas? Surely much more than Google.

Similarly Microsoft. How much is being spent on VR/AR, AI, Cortana, and Microsoft Research? You’ll never know because they’re buried inside of other profitable businesses, but it must be a similar or greater order of magnitude. The difference is in the reporting, not the strategy.

These “bets” are investments! The question that should be asked is whether this money will end up returning on investment in the long run. Here I think there’s much to discuss: The Nest acquisition and tragedy, the wacky science fiction projects. Google’s recent track record of success outside of core areas is certainly questionable. But as a shareholder would you want them to stop trying? Or to fine tune and get better at long-term plays?

Stay tuned for a full analysis in a couple of days.